Mon Dec 28, 2020 by Oppenheim Law on Coronavirus

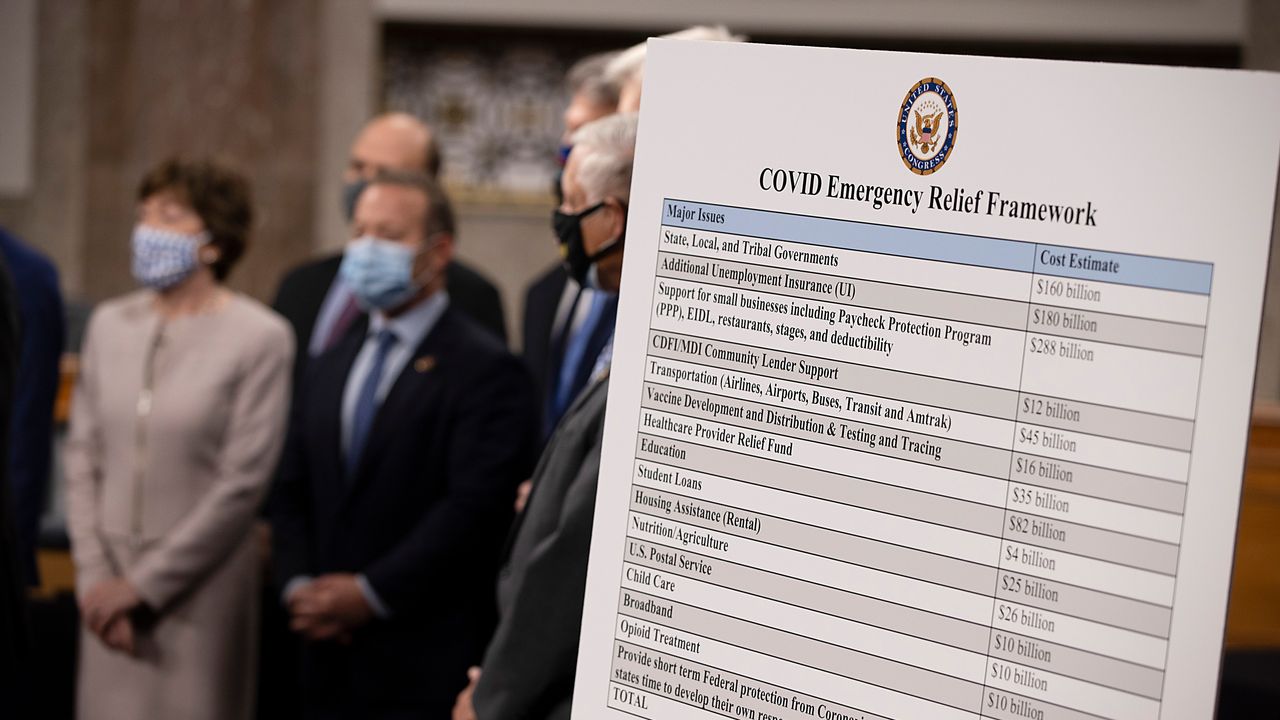

The Consolidated Appropriations Act, 2021 On December 27, 2020 President Trump signed into law the COVID-19 $900 billion relief bill, the Consolidated Appropriations Act, 2021, that Congress passed on December 21,2020. What does this new legislation do? This legislation adds $300.00 to extended weekly unemployment benefits and provides more than $300 billion in aid for small businesses. It also provides […]