Nearly half a year has gone by since Amazon’s new headquarters search was making headlines. However, though the e-commerce giant has yet to declare where its new home will be located, it is important to note that Amazon, along with other e-commerce companies, are shaping how we live. Real Estate Industry and Innovation Back in June, Amazon officially opened its […]

Daylight Saving Time: Helpful or Hurtful? This past Sunday, we changed our clocks ahead one hour to “spring forward” to daylight. Daylight saving time was enacted in the United States after WW1 partially to conserve energy. Back then, incandescent bulbs used a lot of energy, and moving the work day into the day time was thought to be a good […]

Seasoned real estate expert and foreclosure defense attorney Roy Oppenheim reflects on the impact Venezuela’s political crisis will have on South Florida real estate market. Civil unrest creates real estate opportunities With the civil unrest that continues in Venezuela, the question that real estate pundits are having is what impact the current State of Affairs in Venezuela will have on […]

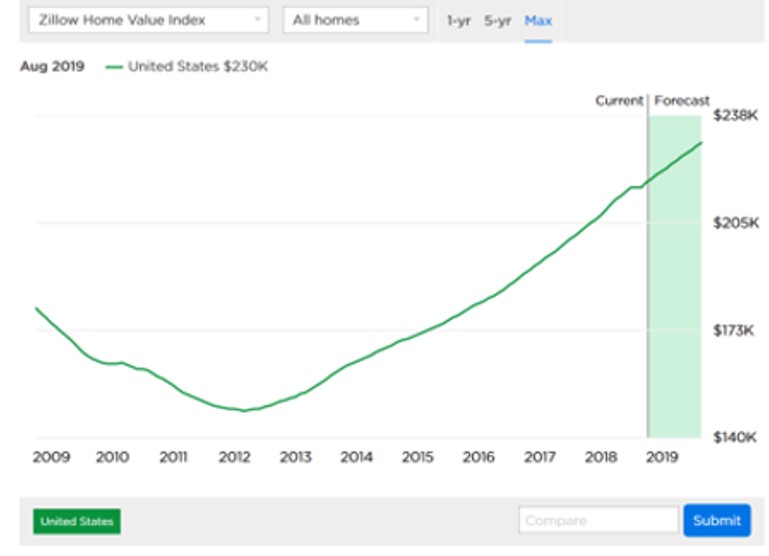

The US real estate market is slowing down. Higher interest rates at 4.75% are dragging real estate sales, as first time home buyers and real estate investors alike are not purchasing at a rate that would stimulate an otherwise seemingly solid economy. Perhaps most telling is that those real estate investors who “fix-and-flip” real estate are sitting on the sidelines […]

Roy Oppenheim’s retrospection on the 10 year Anniversary of the Great Recession. Part two: The unchanged. I started a series of retrospective posts and videos to reflect upon the tenth-year anniversary of the Great Recession. The first post addressed the consequences of the economic collapse. This post discusses what remains the same after it, and in the next, and last […]

Roy Oppenheim Shares What Has Changed & What Hasn’t Changed During the 10-year Great Recession Anniversary Hi, Roy Oppenheim here, real estate attorney, foreclosure defense attorney, and legal blogger for the South Florida Law blog. Folks have been asking me recently what my thoughts are about the 10-year anniversary of the Great Recession and the foreclosure crisis. And I’ve […]

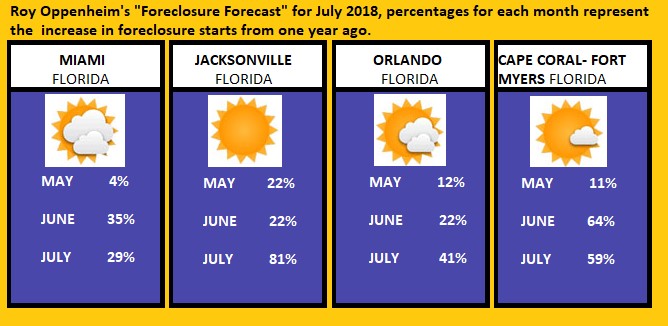

Florida is in the headlines once again. However, this time it’s not because of a hurricane or any other natural disaster. This time, Florida has made headlines for its high rate of foreclosures. According to a study report conducted by Attom Data Solutions, the foreclosure rates are the highest in Florida compared to the last few years. The rates are […]

Politics aside, voters and potential real estate residential home purchasers and sellers are concerned about how the upcoming midterm election and its outcome will affect them financially. With the election having the capacity to change the balance of power, this sense of uncertainty may make selling residential real estate more difficult and cause a delay on purchasing a home until […]