Broker commissions for residential real estate are being challenged. With more and more home buyers relying more on technology for video-tours and neighborhood research, “traditional” real estate commissions are being challenged and yet have largely remained unchanged. Paid by the home seller, the commissions are typically as high as six percent, three percent being paid to the seller’s agent and […]

Article Originally posted on (L to R) Ashley Moody Florida attorney general, Bruce Jacobs, Jacobs Legal and Roy Oppenheim Oppenheim Law (Photos: J. Albert Diaz/ALM, Courtesy Photo) Lawyers who litigated against the company in separate cases criticized the agreement as weak. “While residential foreclosures are at a temporary lull due to federal moratoriums, these moratoriums, just like Florida’s, will come to […]

As many of you know, we at Oppenheim Law were invited to submit a friend of the court brief in the Supreme Court case of Mary Ann Glass v. Nationstar Mortgage in which the issue before the Court was whether a borrower in a foreclosure action is entitled to attorneys’ fees when the borrower successfully disputed the bank’s standing to […]

I just got off the phone with a national housing news reporter. They wanted to know the types of calls we at Oppenheim Law have been fielding from employees who have been furloughed by the unprecedented government shutdown; and the kind of advice we have been giving these individuals. Although I could only speak in generalities under the attorney-client privilege, […]

Fort Lauderdale Foreclosure Defense Attorneys look to ease the government employees affected by the current shutdown by helping them with their foreclosure and housing needs, and deferring payment for such services until they return to work Ellen Pilelsky and Roy Oppenheim, co-founders of Oppenheim Law, announce today that due to the historic government shutdown, their firm will assist government employees […]

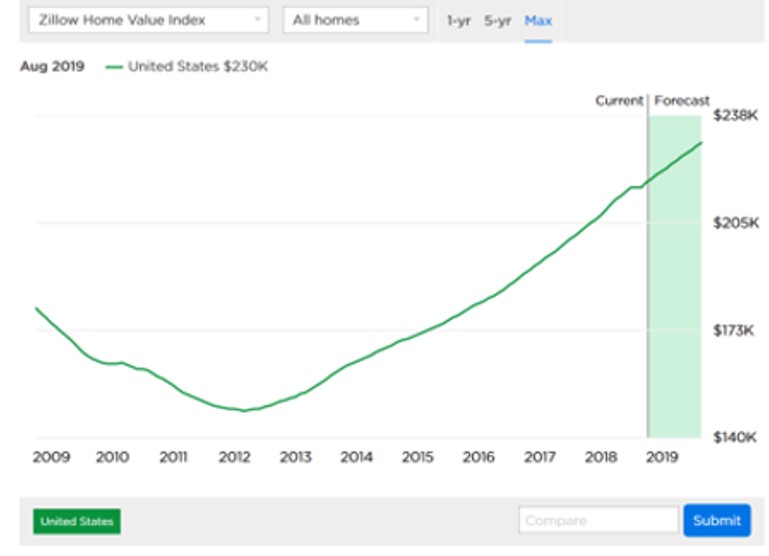

Roy Oppenheim’s retrospection on the 10 year Anniversary of the Great Recession. Part two: The unchanged. I started a series of retrospective posts and videos to reflect upon the tenth-year anniversary of the Great Recession. The first post addressed the consequences of the economic collapse. This post discusses what remains the same after it, and in the next, and last […]

Roy Oppenheim Shares What Has Changed & What Hasn’t Changed During the 10-year Great Recession Anniversary Hi, Roy Oppenheim here, real estate attorney, foreclosure defense attorney, and legal blogger for the South Florida Law blog. Folks have been asking me recently what my thoughts are about the 10-year anniversary of the Great Recession and the foreclosure crisis. And I’ve […]

Roy Oppenheim’s retrospection on the 10 Year Anniversary of the Great Recession Usually anniversaries tend to make us slow down and look back. For us at Oppenheim Law, the anniversary of the start of the Great-Recession of 2008 has been an opportunity to look back, appreciate what we have learned and set new goals for years to come. There […]