“Interest”-ing: Low Rates and Refinancing

Thu Aug 8, 2019 by Oppenheim Law on Loan Modification

Trade Tensions and Stock Scares:

In yet the latest escalation of trade tensions between China and the United States, this past weekend President Trump announced America will impose a 10% tariff on $300 billion of Chinese goods and China responded by suspending its purchase of US agricultural products and lowering the value of the yuan, its currency, to its weakest point since May 20, 2008. The increased retaliation from both countries, coupled with the Federal Reserve bringing interest rates down last week, caused the Dow, a major stock market index, to plunge 900 points and saw the S&P 500 and NASDAQ, also major stock market indices, off by around 2%.

Mortgage Implications:

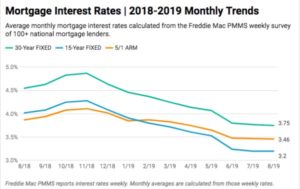

Late last week, these factors made investors flock to the relatively steady bond market, which pushed the yield on the 10-year Treasury down sharply, resulting in lowered interest rates. According to Mortgage News Daily, the average rate on the popular 30-year fixed mortgage hit 3.70% on Friday, the lowest value since November 2016. That rate will presumably lower, as bond yields drop even more.

Simply put, last week’s drop means that over 8 million people who have a 30-year mortgage could qualify for a refinance and even save at least 0.75% off of their current interest rate by doing so. There are several components to contemplate before deciding to refinance.

What to Consider:

A recent CNBC article looks over three factors when analyzing whether refinancing a residential or commercial mortgage makes sense: the ability to earn back investment, the seasoning of the loan, and the impact refinancing will have on other financial goals. Once those points are considered, looking towards the ways to refinance is important as well.

For instance, residential and commercial property owners can refinance using a conventional loan. With property values increasing in many areas, the amount of equity (the difference between your current mortgage and the current market value of your home) one has also increases, which makes it easier for you to refinance. Others can determine whether an FHA (Federal Housing Administration) loan is more suitable, because even if you have little or no equity in your home, a low credit score or higher debt than most lenders generally accept, the FHA guarantees that private lenders will be repaid should you default, which means banks and private lenders make loans that they ordinarily would not at competitive rates that can substantially cut your monthly payments. Furthermore, millions of veterans, as well as those in the National Guard, active duty members, and the reserve, are eligible to refinance with VA (Department of Veteran Affairs) loans.

Here to Help:

At the end of the day, taking advantage of low mortgage interest rates remains an “interest”-ing option for many people. As stated by Ben Grabsoke, president of Black Knight Data and Analytics, “Lower rates have also increased the buying power for prospective homebuyers looking to purchase the average-priced home by the equivalent of 15%, meaning that they could effectively buy $45,000 ‘more house’ while still keeping their payments the same as they would have been last fall.” In other words, increasingly favorable rates allow consumers to both refinance their mortgages and purchase affordable homes, which is definitely something to keep an eye on.

From the Trenches,

Roy Oppenheim

Leave a Reply